UPI payments via ChatGPT are coming: here’s what changes for Indian shoppers

Yes, you may soon tell a chatbot “order my usual veggies” and it will actually buy them—and pay via UPI—without you hopping between apps. NPCI, OpenAI, and Razorpay have kicked off a pilot to let Indians complete e-commerce purchases directly inside ChatGPT. As of October 10–11, 2025 (IST), the integration is live in limited form with early partners like BigBasket and banking rails from Axis Bank and Airtel Payments Bank. The jargon they’re using is “agentic payments.” The gist: you set guardrails, the AI does the boring bits.

What’s happening, exactly?

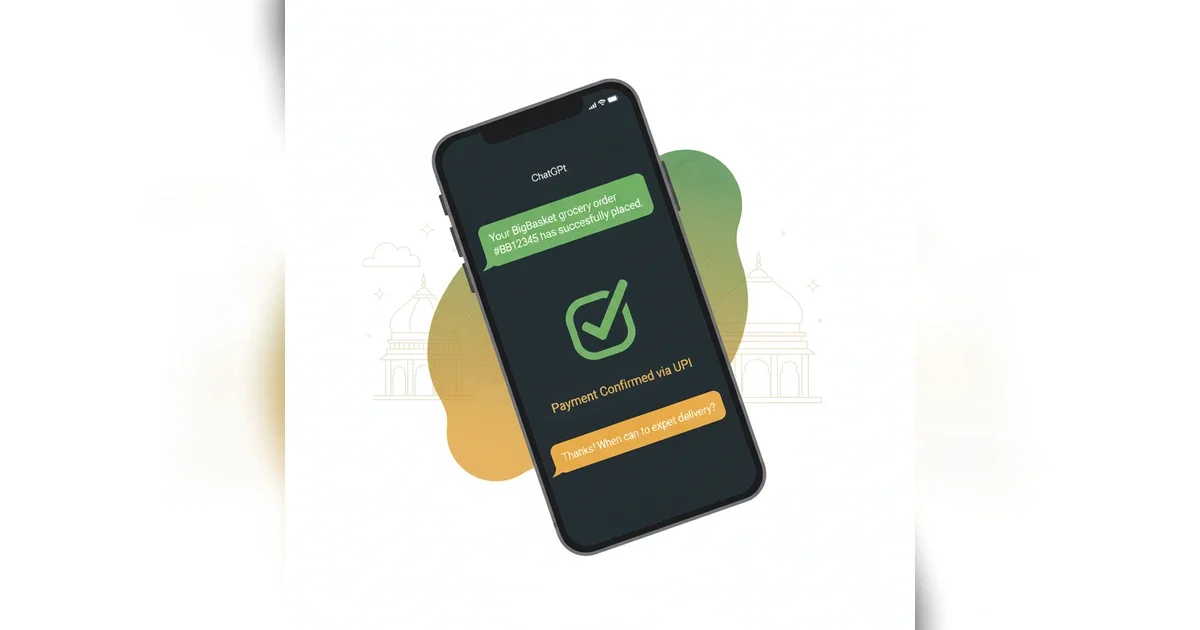

NPCI (the folks who run UPI), Razorpay (payments processor), and OpenAI (ChatGPT’s maker) are piloting a flow where a conversation turns into a checkout. You’ll find a product, confirm the cart, and approve a UPI payment—all in one chat window. Media reports and Razorpay’s own notes suggest pre-authorised, limited-value transactions are supported so ChatGPT can complete routine buys you’ve approved, within caps you control. BigBasket is named as a first merchant in the pilot; more will follow if the trial goes well.

This isn’t a random experiment. UPI runs north of 20 billion transactions a month, and regulators have been nudging the ecosystem towards simpler, safer authentication. Biometric options (face/fingerprint) are also rolling out on UPI this month, which could further smooth the “no-OTP-every-time” experience—useful when an AI agent is the front end.

Short version: India’s payments pipes meet an AI front desk.

Why this matters (beyond the cool demo)

Two pain points get addressed:

1. Friction: Product search → cart → gateway → UPI app bounce is clunky. Chat-first removes app-hopping.

2. Delegation: For low-risk, repeat purchases (milk, mobile recharge, pantry staples), pre-approved caps let the agent finish the job while you carry on with your day.

It’s also a potential template for Indian brands to build conversational storefronts that sit where users already are—inside ChatGPT—without rebuilding checkouts from scratch.

The line to remember: if the pilot sticks, your next “Add to Cart” could be a sentence.

How the flow works (pilot phase)

· Discovery: Chat with ChatGPT to compare products, prices, and availability.

· Cart + Address: The bot confirms items, quantity, delivery slot, and address you select.

· Payment: UPI is the rail. In some cases you may see pre-authorised limits (daily/merchant caps) so routine orders go through with minimal taps; otherwise a standard UPI approval step applies.

· Receipts & Support: Order summary stays in the chat, with links to merchant support.

Behind the scenes, Razorpay stitches the merchant checkout to UPI; NPCI’s infrastructure clears the payment; ChatGPT is the interface and agent.

One sentence summary: think of it as “from chat to checkout” with UPI under the hood.

India lens: availability, partners, and what you can (and can’t) do yet

· Status (IST): Pilot/private beta as of Oct 10–11, 2025. Not a pan-India consumer rollout yet.

· Merchants: BigBasket named first; others likely to join as the pilot expands.

· Banks: Axis Bank and Airtel Payments Bank are participating in trials.

· Auth methods: UPI approval as usual; biometric authentication is being introduced on UPI this month, which could later blend with agentic flows.

· Limits: Expect spending limits and merchant whitelists during pilot. Cross-border is out; this is domestic UPI only.

· Languages: ChatGPT supports multiple Indian languages, but merchant catalog quality varies—expect English + major Indian language coverage first.

Bottom line for now: early, gated access with a clear roadmap; mass availability will depend on pilot results and regulator comfort.

Pros and cons for shoppers

Pros

· Less friction: No app bouncing; discovery to payment stays in one thread.

· Smart repeats: “Order my usual” becomes practical with caps and pre-authorisation.

· Accessible UX: Voice and vernacular support can help non-English users.

· UPI familiarity: Same bank accounts and handles you already use.

Cons

· Trust curve: Letting an AI place and pay needs strong guardrails and clear consent.

· Edge cases: Returns, cancellations, out-of-stock substitutions can get messy in chat.

· Data minimisation: Merchant recommendations vs. user privacy must be transparent.

· Pilot limits: Few merchants/banks at first; not everyone gets access immediately.

Sentence that sticks: convenience is real, but you’ll want tight limits and clear receipts.

Risks and unknowns (read this before delegating payments)

· Regulatory clarity: RBI/NPCI rules on agent-initiated payments will matter—particularly caps, dispute resolution, and liability when an AI misfires. Some features (like pre-authorised UPI “reserve” models) are new; implementation specifics may evolve.

· Security model: Where are consents stored? How are tokens/mandates revoked? What happens on device loss or account compromise? Expect conservative defaults in the pilot.

· Privacy & ads: Will product suggestions be purely contextual or influenced by promotions? The governance around recommendations needs disclosure.

· Availability timeline: No firm public date for general rollout; pilots can expand or stall based on fraud metrics and UX outcomes.

· Biometric reliance: As UPI adds biometrics, inclusivity (device quality, liveness checks), and fallback paths must be watertight.

If you try the pilot, set low spending caps, restrict to trusted merchants, and keep notifications on.

For businesses: why this could be your new storefront

If you sell replenishable or frequently compared items, a conversational funnel could outperform your app’s search bar. Razorpay’s stack abstracts the payment bits; you focus on clean catalogs, transparent pricing, and post-order support scripts in chat. Early movers (think groceries, pharmacy, mobility, bill pay) will gather the best training data and customer habits.

One-liner: commerce shifts to where intent is expressed—in a message, not a menu.

The practical conclusion

Agentic UPI payments inside ChatGPT won’t replace apps overnight, but they’ll chip away at repetitive journeys. If NPCI and RBI are satisfied on safety and consent, expect a broader rollout and more merchants over the next few months. Until then, treat it as a promising beta: great for routine buys, not yet the place for your next TV purchase.