Biometric Authentication for UPI Starts Today: What Indians Need to Know

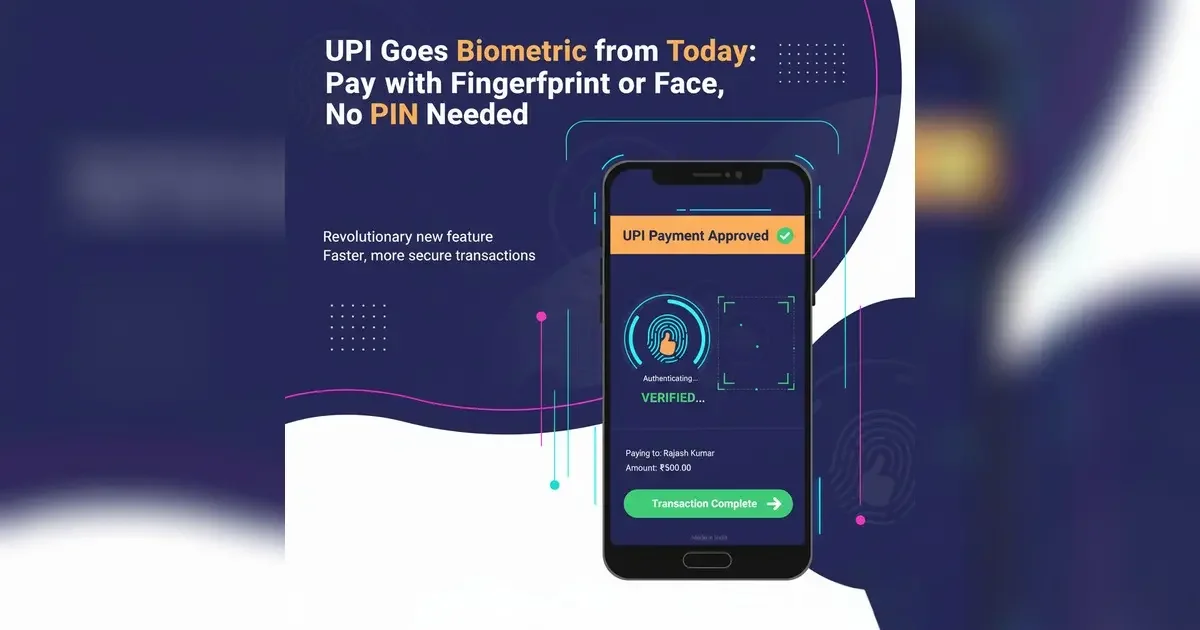

Starting 8 October, Indians can approve UPI payments with a fingerprint or face scan—no PIN needed—thanks to a nationwide rollout led by NPCI and built on the Aadhaar infrastructure. Think of it as UPI learning your face and fingers, so your brain can stop remembering one more number.

This is not a rip-and-replace. PINs still work. Biometrics are an optional second track that banks and UPI apps can enable for you. NPCI’s circular spells out the key guardrails, and there are quite a few—by design.

The headline features (in plain English)

· Pay with your fingerprint or face instead of typing a UPI PIN. Apps will use on-device biometrics (your phone’s secure hardware) to authenticate. Initially, NPCI has capped this at ₹5,000 per transaction, with scope to review later.

· Aadhaar Face Authentication is also being added—but specifically for setting or resetting your UPI PIN (i.e., identity proofing moments), not for every everyday payment.

· This launch is being showcased at the Global Fintech Fest in Mumbai, and major UPI apps are expected to roll it out in phases. Don’t be surprised if your app shows it later in the day or this week.

NPCI and the government are pitching this as a convenience + security upgrade for the 300M+ UPI users who live on their phones. Multiple mainstream outlets, including Reuters, Indian Express, Moneycontrol, and TOI, corroborate the contours of the rollout.

How it will (likely) work in your app

1. Consent first. Your bank/UPI app must ask for explicit consent to turn on biometric payments, and you can opt out any time. Changing devices will require fresh consent.

2. Device check. Apps will verify your phone isn’t rooted/jailbroken and that biometrics are set up at the OS level. If not, you’ll be nudged to register a fingerprint/face in your phone settings.

3. Per-transaction flow. At checkout, instead of a 4/6-digit PIN, you’ll see your phone’s fingerprint or Face ID prompt. For now, expect the ₹5,000 cap to apply when you use biometrics.

4. Safety switches. If you reset your UPI PIN, banks will disable biometric payments until you re-consent. If you go inactive for 90 days, the feature is switched off and needs your confirmation to re-enable. Apps must also rotate keys annually.

Why this is a big deal (beyond the hype)

· Speed & success rates. Fewer failed payments due to mistyped PINs or tiny on-screen keypads—especially on the move or for older users. Reuters and others flag it as a usability win.

· Inclusive for the masses. Aadhaar’s ubiquity means biometric verification is familiar in India; marrying it to UPI reduces friction for first-time or infrequent users at kirana counters or BC outlets.

· Security with nuance. On-device biometrics keep the sensitive data inside your phone’s secure enclave; NPCI’s rules add multiple circuit-breakers (consent, inactivity auto-off, device checks). That’s a pragmatic blend of convenience and control.

The trade-offs you should actually think about

· Availability will be staggered. Your bank or app (PhonePe, Paytm, GPay, etc.) may need a few updates before you see the toggle. Treat it as a phased rollout.

· The ₹5,000 ceiling matters. For larger spends, you’ll likely still use your PIN until NPCI revisits limits after monitoring fraud and performance data.

· Shared phones are tricky. If multiple family members use one handset, the person whose biometrics are enrolled could unintentionally approve payments. Set app-level controls and avoid enrolling extra fingerprints casually. (This is a general security best practice; the on-device model raises the stakes.)

· Privacy optics. Everyday payments use on-device biometrics; Aadhaar face authentication is reserved for PIN set/reset and follows UIDAI rules. Knowing that difference is important in the current privacy conversation.

Quick start checklist (for you/your parents)

· Update your UPI app to the latest version.

· Turn on biometric lock at the phone level (Settings → Security).

· In the UPI app, look for “Biometric payments” or similar; read and accept the consent notice.

· Test with a small transaction (under ₹5,000).

· If you change phones or reset your PIN, expect to re-enable biometrics.

UPI’s biometric turn is a measured upgrade, not a reckless leap. Optional, capped, and consent-driven—this is India nudging digital payments towards what feels natural in 2025: you are your password. Expect a few rough edges in week one, but the direction is clear—and very Indian in its scale and pragmatism.