Swiggy Just Loaded a ₹10,000 Crore War Chest. The Quick Commerce Battle Gets Real.

Here's the thing about cash-burning wars—the side with deeper pockets doesn't always win, but the side that runs out of money always loses.

On December 12, 2024, Swiggy closed one of the largest qualified institutional placements (QIP) in Indian consumer tech history. ₹10,000 crore ($1.18 billion) from heavyweight investors including Singapore's GIC and Temasek, BlackRock, Goldman Sachs Asset Management, and every major domestic mutual fund from SBI to HDFC. The company allotted 26.66 crore equity shares at ₹375 per share—a 3.97% discount to the floor price of ₹390.51.

This isn't just fundraising. This is Swiggy's declaration that the quick commerce war is far from over, even if Zomato's Blinkit currently holds the commanding heights.

The Money Trail: Where ₹10,000 Crore Actually Goes

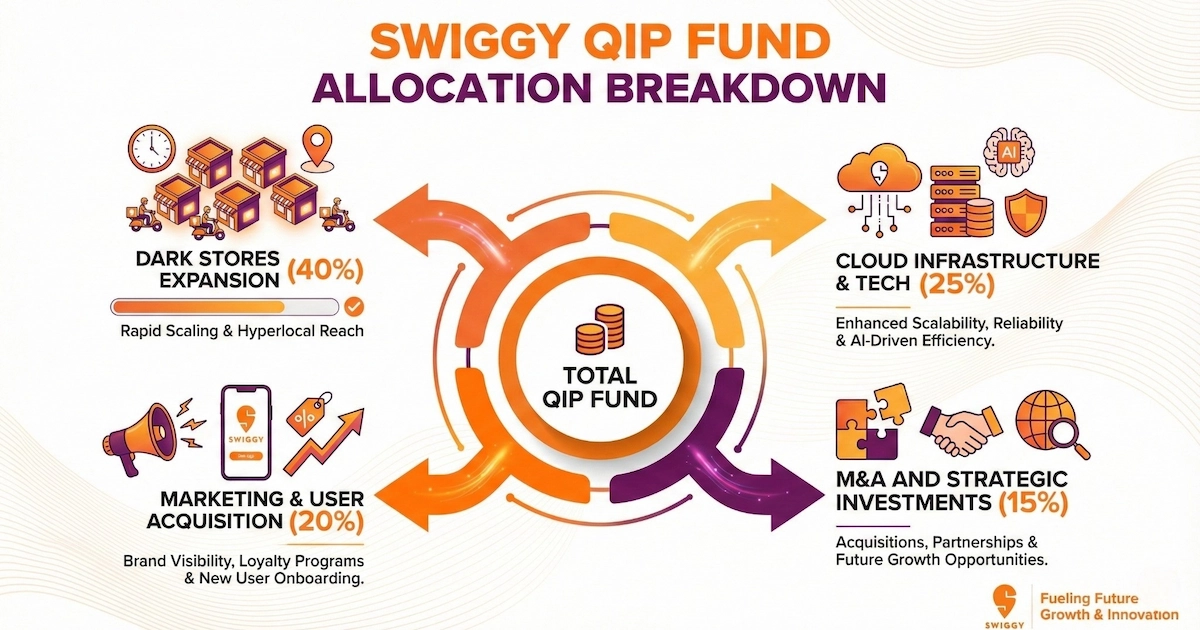

Swiggy's regulatory filings reveal a clear deployment strategy, and the priorities tell the whole story.

₹4,475 crore—the single largest allocation—goes directly into expanding Swiggy's quick commerce fulfilment network. Dark stores, warehouses, and the logistics infrastructure that powers Instamart. The plan: grow the fulfilment footprint from approximately 5 million square feet (as of November 30, 2024) to 6.7 million square feet by December 2028.

₹3,300+ crore is earmarked for cloud infrastructure and brand marketing over the next three years. Swiggy's current cloud services agreement expires in February 2026, and the company has already signed a letter of intent for a ₹1,820 crore cloud commitment.

The remaining funds target technology investments and what the company calls "inorganic growth opportunities"—acquisition-speak for buying smaller players or strategic assets if opportunities emerge.

Why Now? The Competitive Pressure Is Real

Let's call the situation what it is: Swiggy is playing catch-up.

Zomato's Blinkit currently commands approximately 45% market share in quick commerce, per recent industry estimates. Swiggy's Instamart sits at around 27%. Zepto holds 21% and counting. The gap isn't narrowing on its own.

Consider the numbers from Q4 FY25:

- Blinkit: 1,301 dark stores, processing approximately 15.7 lakh daily orders

- Instamart: 705 dark stores (as of December 2024), handling around 12.15 lakh daily orders

- Average Order Value: Blinkit at ₹665 vs Instamart at ₹527

Goldman Sachs valued Blinkit at a staggering $13 billion earlier this year—higher than Zomato's core food delivery business. That's a six-fold increase from $2 billion in March 2023. Meanwhile, Zomato recently pumped another ₹1,500 crore into Blinkit in February 2025 to maintain its expansion pace.

Zepto, the scrappy startup founded by Stanford dropouts, raised $1.35 billion in 2024 alone across multiple rounds, maintaining a $5 billion valuation. The company plans to file its IPO DRHP in early 2025.

Swiggy's ₹10,000 crore QIP isn't an offensive move. It's survival capital for a war of attrition.

The Instamart Inflection Point

There's cautious optimism buried in Swiggy's earnings calls, and it centres on Instamart's path to profitability.

CEO Sriharsha Majety has publicly stated that Swiggy expects contribution breakeven for Instamart by Q3 FY26 (October-December 2025) and adjusted EBITDA breakeven for the consolidated company by Q4 FY25. The company's top seven cities for Instamart are already contribution-positive, with 75% of stores in these cities hitting profitability.

How? Three levers:

First, advertising revenue. FMCG giants are increasingly looking at quick commerce platforms as advertising channels. Swiggy expects advertising to contribute 6% to Gross Order Value at steady state—a significant margin boost.

Second, the mega-pod strategy. Unlike competitors racing to open maximum dark stores, Swiggy is building larger facilities (8,000-10,000 sq ft) called "mega dark stores" that support broader product assortment and staggered delivery timelines (10 minutes for grocery, 20 minutes for larger items). CFO Rahul Bothra claims Swiggy has "created sufficient capacity on the dark store network to easily double our business from here without having the need to add more stores."

Third, non-grocery expansion. Non-grocery items now account for 26% of Instamart sales, up from just 9% a year earlier. Electronics, fashion, pharmacy, and general merchandise carry better margins than groceries.

The Dilution Question

Investors should acknowledge what's happening here. This QIP represents approximately 10% dilution for existing shareholders—barely 13 months after Swiggy's November 2024 IPO that raised ₹4,500 crore.

That's aggressive equity issuance by any measure. Swiggy's stock is down roughly 20% from its 52-week high of ₹617.30 (hit in December 2024), trading around ₹416 at the time of QIP close.

The institutional demand was undeniable—over 4x oversubscription with 61 investors receiving allocations from 80+ bids. But retail investors who bought during the IPO are watching their ownership get diluted while profitability remains a future promise.

The counter-argument: without this capital, Swiggy might lose the quick commerce war altogether. In winner-take-most markets, second place often means irrelevance.

The Zomato Paradox

Here's what makes this competition fascinating. Zomato isn't sitting still, but it's also not invincible.

Zomato shut down its 10-minute food delivery pilot "Zomato Quick" in late 2024, citing profitability concerns and inconsistent customer experience. CEO Deepinder Goyal acknowledged that "the current restaurant density and kitchen infrastructure is not set up for delivering orders in 10 minutes."

Meanwhile, Swiggy's Bolt 10-minute food delivery service has scaled to over 500 cities and accounts for 10% of all food orders—growing while Zomato retreats from the same category.

Zomato's overall revenue for FY25 stands at ₹20,243 crore with a profit of ₹527 crore. Swiggy's FY25 revenue is ₹15,227 crore with a loss of ₹3,117 crore. The gap is significant, but Swiggy's revenue is growing at 35% while improving its loss trajectory.

What the Smart Money Is Watching

The participation of GIC, Temasek, BlackRock, and Goldman Sachs isn't just validation—it's a signal that institutional investors see a viable path to returns despite current losses.

The thesis goes something like this: India's quick commerce market is projected to reach $42 billion by 2030 (Morgan Stanley estimates). The sector grew 77% annually during its pandemic-era surge and continues expanding. Even capturing 25-30% of this market makes Swiggy's Instamart worth multiples of current implied valuations.

But execution matters. Analyst price targets for Swiggy range wildly—from ₹290 to ₹740—reflecting genuine uncertainty about whether management can convert capital into sustainable competitive advantage.

The Uncomfortable Truth

Quick commerce in India has entered a phase where capital efficiency matters more than capital access. Swiggy, Zomato, and Zepto all have billions in war chests. The question is no longer who can raise money, but who can convert money into profitable market share.

Swiggy's mega dark store strategy, non-grocery pivot, and measured store expansion suggest management understands this. The company isn't trying to out-spend Blinkit store-for-store. It's betting that operational efficiency and category expansion will win over sheer footprint.

Whether that bet pays off depends on factors no amount of capital can fully control—consumer behaviour, regulatory shifts, and whether 10-minute delivery of everything from groceries to electronics remains a sustainable business or a subsidized convenience that customers love but nobody can monetize.

The Bottom Line

Swiggy's ₹10,000 crore QIP isn't the end of the quick commerce story. It's the reset button that ensures Swiggy stays in the game long enough to find out how the story ends.

For investors, the calculation is straightforward but not simple: Do you believe Swiggy can close the gap with Blinkit while turning Instamart contribution-positive within the next 12-18 months? If yes, current valuations might represent opportunity. If not, the dilution just bought you a front-row seat to expensive competition.

The company plans to expand Instamart's fulfilment network to 6.7 million square feet by 2028 and expects consolidated EBITDA breakeven by late 2025. Those timelines will either validate management's strategy or become excuses for why more capital is needed.

Quick commerce in India is a $6-7 billion market today, racing toward $40+ billion by decade's end. Swiggy just bought its ticket to compete for that future. Whether the ticket was priced right remains the billion-dollar question.

We'll update this analysis when Swiggy releases its next quarterly results.