The $800 Billion Number That Just Changed Everything

SpaceX CFO Bret Johnsen sent a letter to shareholders on December 12, 2025, that effectively rewrote the rules of private company valuations. The message was straightforward: SpaceX has approved an insider share sale at $421 per share, valuing Elon Musk's rocket and satellite company at approximately $800 billion.

That's double the $400 billion valuation from just six months ago. It vaults SpaceX past OpenAI's $500 billion October valuation, making it the world's most valuable private company. And perhaps most significantly, it confirms what industry watchers have suspected for months—SpaceX is actively preparing for a 2026 IPO that could become the largest public offering in history.

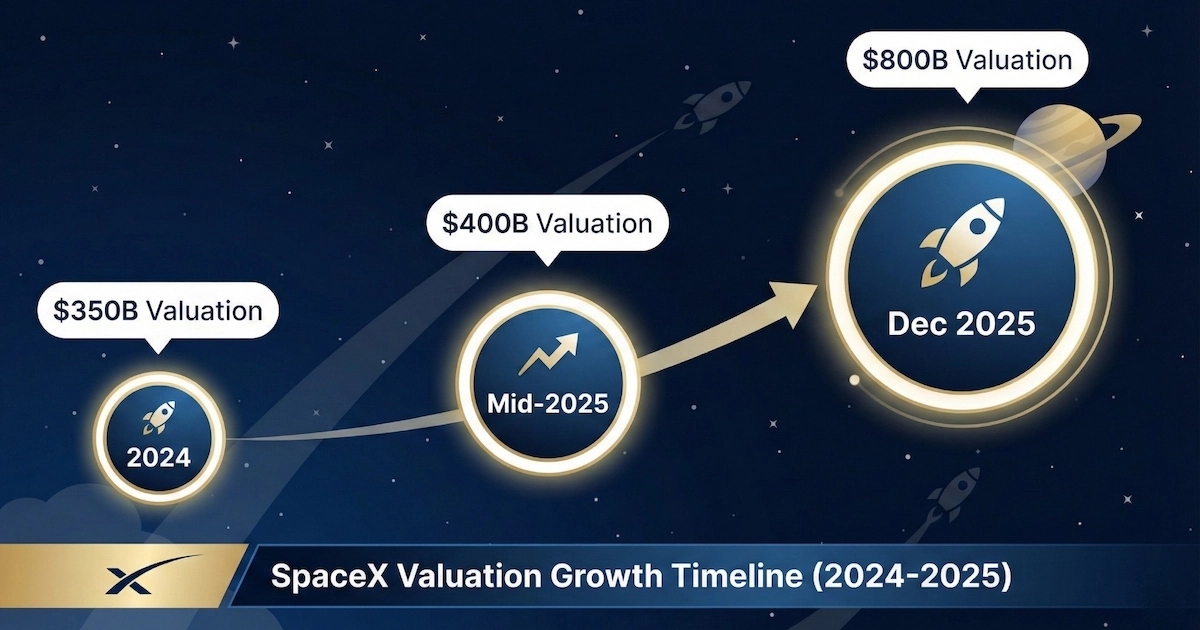

The trajectory here is genuinely remarkable. In 2024, SpaceX was valued at roughly $350 billion. By mid-2025, that figure hit $400 billion. Now, in December 2025, we're looking at $800 billion. That's a 128% increase in about 18 months for a company that's been around since 2002.

What's Actually Driving This Valuation

Let's be direct about what's happening here. This isn't speculative hype divorced from business fundamentals—though the multiples are certainly aggressive.

Starlink has become a cash machine. The satellite internet division now serves over 8 million subscribers globally, up from 1 million in December 2022. Revenue projections for 2025 sit around $11-15 billion, with Starlink contributing roughly 75% of that total. The service operates through more than 7,500 satellites in low Earth orbit—the largest active satellite constellation ever deployed.

The launch business remains dominant. SpaceX has conducted over 160 Falcon 9 missions in 2025 alone, accounting for approximately 80% of all global orbital launches. No competitor comes close to matching this cadence, and the company's reusable rocket technology has fundamentally altered launch economics industry-wide.

Government contracts provide stability. NASA, the Department of Defense, and various intelligence agencies represent a meaningful revenue stream, though Musk has publicly stated that government work will constitute less than 5% of SpaceX revenue by 2026. The Starshield military variant of Starlink—extensively deployed in Ukraine—represents a growing defense sector opportunity.

Direct-to-cell spectrum acquisition changes the game. SpaceX recently purchased over $17 billion in wireless spectrum licenses from EchoStar, enabling standard smartphones to connect directly to Starlink satellites without specialized equipment. This partnership with T-Mobile essentially transforms Starlink from a rural broadband solution into a potential global mobile carrier competitor.

The IPO Numbers Are Staggering

According to Bloomberg reporting confirmed by Musk himself, SpaceX is targeting a 2026 IPO—potentially as early as June—that would raise significantly more than $30 billion. The company is eyeing a valuation between $1 trillion and $1.5 trillion, which would place it near Saudi Aramco's $1.7 trillion market cap during its record 2019 listing.

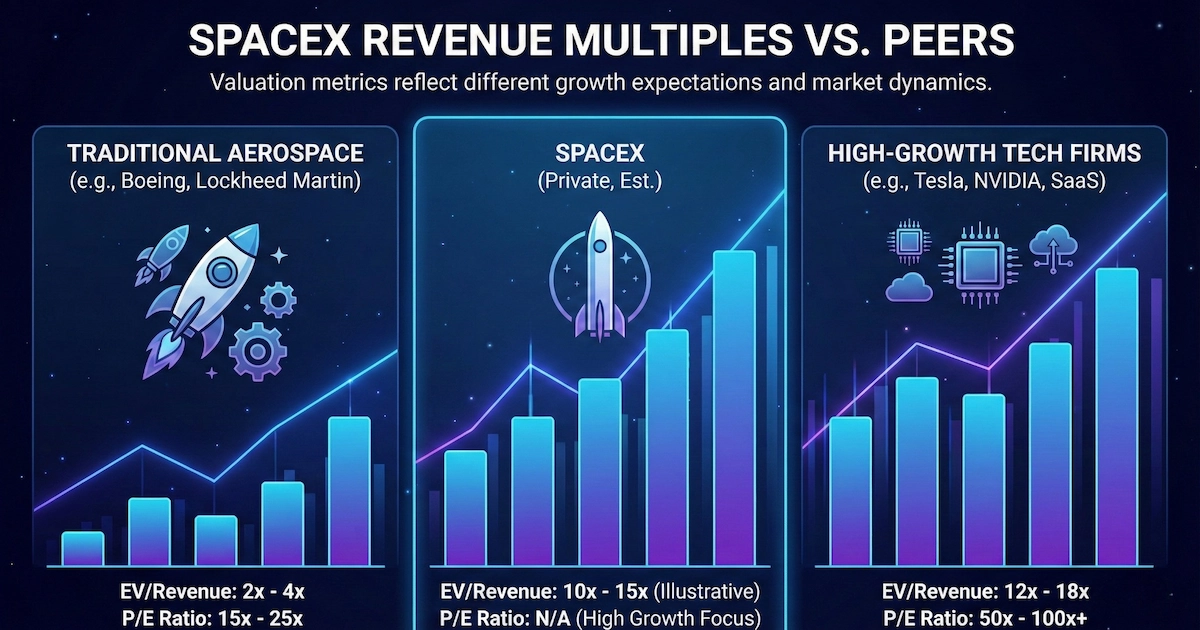

Here's where the math gets interesting. SpaceX expects revenue between $22 billion and $24 billion in 2026. At an $800 billion valuation, that's roughly 35x forward sales. At $1.5 trillion, you're looking at 62-65x revenue.

For context: Palantir Technologies, one of the market's most aggressively valued tech companies, trades at about 70x sales. Mature aerospace primes like Boeing, Lockheed Martin, and Airbus trade in single-digit EV/EBITDA multiples. SpaceX isn't being valued like a defense contractor—it's being priced like a high-growth tech platform with monopolistic characteristics.

Why Musk Changed His Mind About Going Public

For more than a decade, Musk consistently argued against taking SpaceX public. His reasoning was straightforward: quarterly earnings pressure would compromise long-term engineering projects, particularly the capital-intensive, failure-tolerant development of reusable rockets and, eventually, Mars colonization infrastructure.

So what changed?

Starlink's revenue is now "smooth and predictable"—the exact threshold Musk publicly set years ago for considering an IPO. The business has achieved genuine scale and recurring revenue characteristics that public investors can model.

Cash flow is positive. Musk stated on X that "SpaceX has been cash flow positive for many years," eliminating the existential funding pressure that once made private capital essential for survival.

The capital requirements are massive. SpaceX's stated ambitions include an "insane flight rate" for Starship, AI data centers in space, and a base on the moon. These projects require billions in upfront investment that even successful secondary share sales can't sustainably provide.

Tesla shareholders deserve access. At a November meeting, Musk said he wanted to "figure out some way for Tesla shareholders to participate in SpaceX." An IPO accomplishes this directly, potentially creating a loyalty-based investor base that understands Musk's long-term operational philosophy.

The Space-Based AI Data Center Thesis

Buried within SpaceX's IPO preparation is perhaps the most audacious element of the valuation case: orbital artificial intelligence infrastructure.

In a company memo, SpaceX indicated that IPO proceeds would fund the development of space-based data centers using chips installed in upgraded Starlink V3 satellites. Musk has claimed that Starship could deliver "around 300 GW per year of solar-powered AI satellites to orbit, maybe 500 GW."

To put that in perspective: total global data center capacity currently sits around 59 gigawatts on Earth. Musk's stated target would potentially deliver eight times Earth's current capacity annually.

The thesis is compelling on paper. Orbital data centers would have access to unlimited solar power, natural cooling in the vacuum of space (up to 40% of terrestrial data center energy consumption goes to cooling), and freedom from the permitting and power grid constraints plaguing ground-based facilities. Google, Blue Origin, and multiple startups are pursuing similar visions.

Whether this becomes a meaningful revenue line by 2030—or remains an aspirational concept—will significantly influence whether SpaceX's IPO valuation proves justified.

What Could Go Wrong

Let's be honest about the risks, because they're substantial.

Execution risk on Starship. The super-heavy launch vehicle has experienced "several explosive setbacks during uncrewed test flights in 2025," per CNN reporting. Starship must transition from test flights to reliable commercial operations, especially for NASA lunar missions. Delays or failures would pressure both revenue projections and valuation multiples.

Competition isn't standing still. Amazon's Project Kuiper has begun launching satellites. OneWeb continues expanding. Traditional carriers and 5G networks may erode satellite internet demand in urban markets where terrestrial options are superior. The direct-to-cell opportunity faces regulatory hurdles in markets with strict data sovereignty requirements.

Governance concerns are legitimate. Musk currently serves as CEO of Tesla and SpaceX, owns majority stakes in xAI and X (formerly Twitter), and heads initiatives including Neuralink and The Boring Company. Institutional investors will scrutinize whether he can effectively lead two massive public companies simultaneously while managing multiple other ventures.

Public market pressures are real. SpaceX's experimental, failure-tolerant approach to rocket development—blowing up prototypes to learn quickly—is easier to justify in private boardrooms than on quarterly earnings calls. As Cornell professor Mason Peck noted: "Will they become the same as any other aerospace company and ultimately mired in conservatism and legacy solutions? That's entirely possible."

The valuation is aggressive. Even bullish analysts acknowledge that 35-65x revenue multiples require extraordinary profitability assumptions far exceeding current demonstrated margins. A "WeWork moment"—where public investors reject private market valuations as disconnected from reality—remains possible.

What This Means for Musk's Wealth

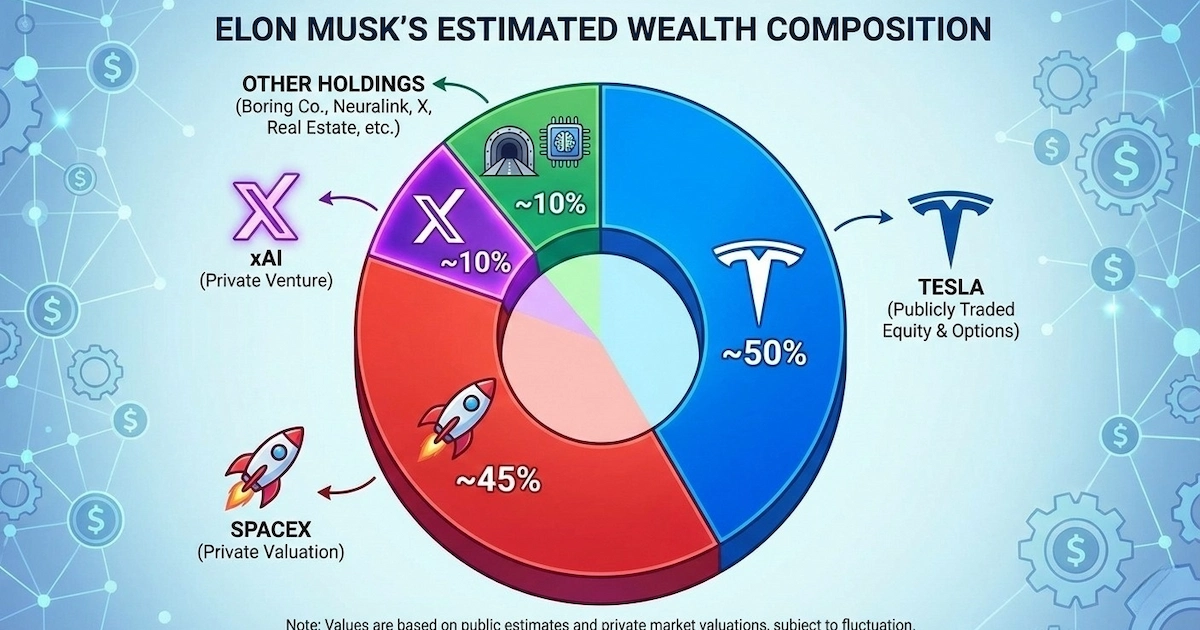

The personal financial implications are straightforward. Musk owns approximately 42% of SpaceX. At the current $800 billion private valuation, that stake is worth roughly $336 billion. At a $1.5 trillion IPO valuation, it would exceed $625 billion.

According to Bloomberg's Billionaires Index, Musk's current net worth sits around $461 billion, with most of that attributable to Tesla holdings. A successful SpaceX IPO could more than double his fortune, cementing his position as the world's wealthiest individual by a margin that would be historically unprecedented.

The Investor Access Problem

Here's the uncomfortable reality for most investors: you still can't buy SpaceX directly, and you may face challenges doing so even after the IPO.

SpaceX's existing shareholder base—Founders Fund, Fidelity, Google, Valor Equity Partners, and various sovereign wealth funds—isn't particularly diverse. If the company adopts a dual-class share structure (common among tech IPOs), Musk could retain majority voting control while offering minority economic participation.

Current indirect exposure options include:

- XOVR ETF – A crossover fund that explicitly holds private SpaceX shares among other late-stage ventures

- Destiny Tech100 (DXYZ) – A closed-end fund with SpaceX exposure, though highly volatile

- Alphabet (GOOGL) – Google owns approximately 7% of SpaceX through its investment arm

- Fidelity mutual funds – Various Fidelity products hold SpaceX positions

None of these provide pure-play exposure, and each carries its own risk profile.

The Broader Market Implications

SpaceX's IPO, if executed at scale, could catalyze a wave of mega-listings. Bloomberg estimates that as much as $2.9 trillion worth of private companies could go public in 2026, including potential offerings from Databricks, Anthropic, and others.

This challenges a decade-long trend of staying private longer. Companies like SpaceX, Stripe, and ByteDance have attracted valuations in private rounds that dwarf most public companies—all without quarterly financial reporting scrutiny. A successful SpaceX listing would represent a powerful endorsement of returning to public markets.

The space industry itself stands to benefit from increased investor attention. EchoStar's stock jumped as much as 18% on SpaceX valuation news. Rocket Lab extended gains. The sector, worth $630 billion in 2023, is projected to triple by 2035.

What Happens Next

Several milestones will determine whether the 2026 IPO timeline holds:

Formal SEC S-1 filing – This will reveal detailed financials, governance structures, risk factors, and share class arrangements. It's the definitive signal that listing preparation is serious.

Secondary share sale completion – The $2.56 billion insider transaction currently underway will establish pricing dynamics and investor appetite.

Starship operational progress – Achieving consistent, reliable super-heavy launches would validate the most bullish revenue projections.

Starlink profitability metrics – Subscriber growth, churn rates, and margins will determine whether the division deserves its outsized valuation contribution.

The IPO could slip to 2027 depending on market conditions, regulatory requirements, or Musk's evolving strategic priorities. But the direction of travel is clear. After two decades as the most valuable private company never to go public, SpaceX appears genuinely committed to offering Wall Street a seat on the rocket ship.

Whether that ride justifies an $800 billion ticket price—let alone $1.5 trillion—remains the question that will define one of the most consequential IPOs in market history.