Shiprocket IPO 2025: Why the Logistics Giant is Following Swiggy to the Bourse

Here is the brutal truth about the Indian startup ecosystem in late 2025: The days of easy VC money are dead. Buried. Gone.

If you are a late-stage startup founder in Bengaluru or Gurugram today, you have two choices. You can either beg existing investors for a down-round (valuation cut) to keep the lights on, or you can suit up, ring the bell at Dalal Street, and ask the public for cash.

Shiprocket, India's largest e-commerce shipping enabler, has chosen option two.

Fresh off the heels of Swiggy’s market debut in late 2024 and the very recent listing of Meesho just days ago (December 10, 2025), Shiprocket is gearing up for its own ₹2,500 Crore initial public offering. They have the SEBI approval, they have the narrowed losses, and frankly, they might not have a better alternative.

Let’s break down what this means for the market, for the company, and for you.

The Big Picture: Public is the New Private

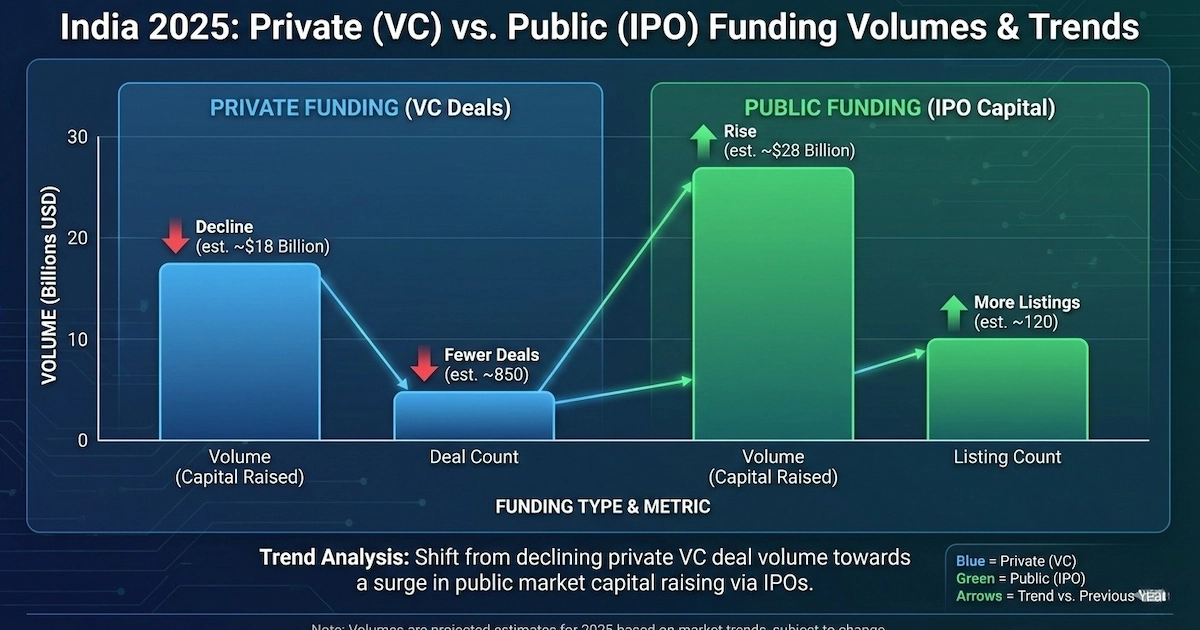

To understand why Shiprocket is listing now, you have to look at the money.

Throughout 2025, private funding in India has taken a nosedive—down nearly 25% in the first half of the year compared to 2024. The "Funding Winter" has frozen the big $100 million checks that used to fly around like confetti. But the public markets? They are practically overheating.

Swiggy cracked the door open in November 2024. Meesho kicked it down earlier this week with a listing that saw a 53% pop on day one. Investors are showing they have an appetite for Indian tech, provided the companies aren't burning cash like it's 2021.

The Shiprocket Plan

Shiprocket isn't just "thinking" about this. They are locked and loaded.

- IPO Size: ~₹2,500 Crore ($300 Million approx)

- Structure: A mix of Fresh Issue (money for the company) and Offer for Sale (OFS - money for early investors to exit).

- Approval Status: SEBI gave the nod in late October 2025.

- Valuation: Expected around $1.2 - $1.5 Billion (₹10,000 - ₹12,500 Crore).

Note: Shiprocket filed a confidential Draft Red Herring Prospectus (DRHP), a relatively new route that allows companies to keep their cards close to their chest until approval.

The Financials: Cleaning Up for the Guests

You can't invite the public to your house if it's a mess. Shiprocket spent FY25 tidying up their balance sheet, and the results are... actually decent.

Metric | FY 2024 (The Mess) | FY 2025 (The Cleanup) | Change |

Operating Revenue | ₹1,316 Cr | ₹1,632 Cr | ▲ 24% |

Net Loss | ₹595 Cr | ₹74 Cr | ▼ 88% (Improvement) |

Cash EBITDA | -₹128 Cr (Loss) | +₹7 Cr (Profit) | Turned Positive |

The "So What?"

The revenue growth (24%) is healthy, but the real story is the loss reduction. Slashing losses from nearly ₹600 Cr to just ₹74 Cr is a massive signal to investors that the company isn't a bottomless pit. Achieving positive Cash EBITDA (earnings before interest, taxes, depreciation, and amortization) is the magic password for institutional investors in 2025.

They achieved this by cutting ESOP costs and optimizing their "burn"—tech speak for spending less money to make money.

Why Should You Care? (The Bull Case)

Shiprocket isn't just a courier company; they are the "operating system" for Indian e-commerce. If you've ever bought something from a D2C brand on Instagram or a small website, Shiprocket likely handled the backend.

- The "Zomato" Factor: Zomato owns a significant chunk of Shiprocket. Zomato has been one of the best-performing tech stocks of the last two years. If Zomato trusts them, the market likely will too.

- Diversification: They aren't just shipping boxes anymore. Their newer verticals—cross-border shipping, checkout services, and marketing tools—now contribute nearly 20% of revenue. They are building a moat.

- The India Story: E-commerce in Tier-2 and Tier-3 cities is still exploding. Shiprocket is the shovel-seller in this gold rush.

The Risks: What Experts Disagree On

It’s not all sunshine and listing gains. I spoke to a few analysts (off the record), and here is where the skepticism lies.

1. The "Path to Net Profit" Question

Sure, Cash EBITDA is positive. But Net Profit is still negative (-₹74 Cr). Public markets in India are notoriously unforgiving of loss-making companies when the market mood swings. If the broader market dips in early 2026, Shiprocket could be punished for those red ink numbers.

2. The Low-Margin Trap

Logistics is a brutal business. You are fighting for pennies on every delivery. Unlike a SaaS company with 80% margins, logistics companies often operate on razor-thin margins. Shiprocket is an aggregator—they don't own the planes or trucks (mostly)—which protects them from asset heaviness but leaves them vulnerable to price hikes from courier partners like Blue Dart or Delhivery.

3. The "OFS" Heavy Weight

A large chunk of this IPO (over ₹1,000 Cr) is likely to be an Offer For Sale (OFS). This means existing investors are cashing out. While normal, a heavy OFS can sometimes signal that the "smart money" thinks growth has peaked.

Conclusion: The Verdict

Shiprocket's IPO is a symptom of the times. The company has matured, disciplined its spending, and is now forced to graduate to the public markets because the private ones are closed for the season.

If you believe in the Indian D2C (Direct-to-Consumer) story, Shiprocket is a proxy bet on that entire sector. They don't need one brand to win; they just need any brand to ship.

My take? Watch the final pricing. If they get greedy with the valuation (north of $2 Billion), stay away. If they price it sensibly (around $1.2 - $1.4 Billion), it could be a solid portfolio diversifier.