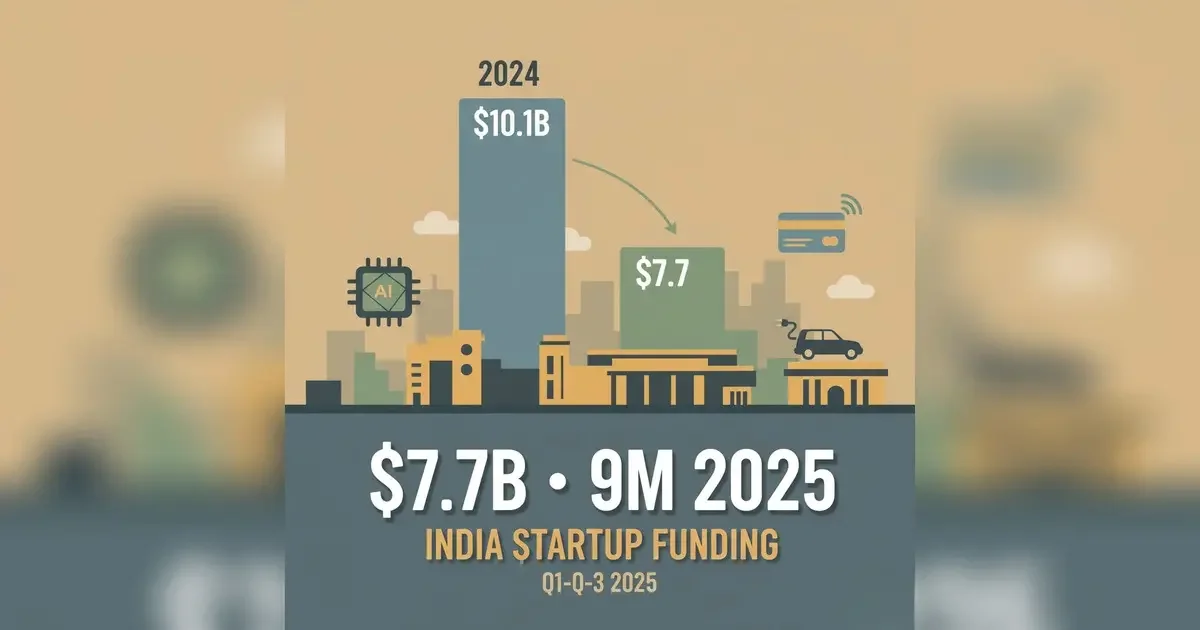

Here’s the uncomfortable truth no founder wants to hear: money has moods. In 2025, India’s tech funding mood swung from FOMO to “show me the metrics.” Indian startups pulled in $7.7 billion in the first nine months of 2025, a drop of roughly 24% year-over-year—and miles below the 2021 sugar high. That’s not the apocalypse. It’s the market asking tougher questions—and expecting grown-up answers.

Yet, even in a year of tighter belts, India still sits in the global big leagues. By one major tracker’s cut of the numbers, India was the third-most funded country in 9M 2025, behind only the U.S. and the U.K. Translation: the pie got smaller, but we’re still getting a large slice.

What the $7.7B actually says

If you’re building in India, this slowdown is less about doom and more about normalization. The froth has cleared. Late-stage mega rounds are rarer, down-rounds aren’t taboo, and “profit path” has gone from slide 23 to slide 3 in every pitch. The headline number—$7.7B—captures this vibe shift cleanly: lower volumes, higher scrutiny, fewer spray-and-pray bets. Business Standard’s read on the data shows the pullback versus 2024, and also notes that only a handful of names have cracked the $100M+ club this year. That’s a smaller club than founders would like, but it forces discipline we frankly needed.

The paradox of strength in a slowdown

Here’s the paradox: funding is down, but India’s ecosystem position is strong. On the ground, Bengaluru is still a gravitational field for talent and capital. In fact, Startup Genome’s 2025 report shows Bengaluru-Karnataka climbing into the global Top 20, at #14, a leap that tells you what investors already know: the pipeline of credible founders, operators, and repeat angels here is deep. When cities move up while dollars dip, it usually means resilience—not fragility.

Zoom out further and you’ll see policy scaffolding still in place: DPIIT-recognized startups have crossed the 1.5-lakh mark, and the “third-largest startup ecosystem” line isn’t just a slogan—it’s a policy anchor that’s steadily compounding. None of that immunizes us from cycles, but it does cushion the fall.

Why the money cooled (and what to do about it)

1) The late-stage winter: Global growth funds are being picky. They’re protecting portfolio companies and pricing risk into term sheets. If you’re Series C+, think extension, not expansion.

2) Regulatory reality checks: Fintechs especially are feeling it. When rules tighten, capital waits. It’s not personal; it’s risk management.

3) AI crowd-out: Money is chasing model-heavy plays and infrastructure layers. If you’re not clearly AI-native (or AI-augmented), your multiple probably compressed.

What helps now? Ruthless prioritization. Build for gross margin, not vanity MAUs. Compress payback periods. And don’t be cute with governance—tight cycles punish loose controls.

The bright spots hiding in plain sight

Even with smaller cheques, quality deals are getting done—particularly in climate/EV supply chains, healthcare ops, and fintech infra. Business Standard flagged names like Erisha E Mobility, GreenLine, Infra.Market, Access Healthcare, and Groww among the larger 2025 raises. That mix tells a story: capital is tilting toward real-economy rails and platforms with clean unit economics. If your pitch smells like durable cash flow, the door is still open.

For founders: a practical playbook for Q4 and 2026

· Default alive, not default hopeful. Extend runway to 18–24 months. If you can’t, re-plan until you can.

· Lift price or lift value—ideally both. Indian customers pay when they clearly win—cut “nice-to-have” fluff.

· Treat AI like compounding, not cosplay. If AI meaningfully drops your COGS or boosts LTV, integrate it. If not, skip the buzzwords.

· Bake in compliance early. Especially for fintech, health, logistics—regulatory flu can knock you out mid-round.

· Recruit for operators, not just storytellers. The next up-cycle rewards teams who can actually turn the dials.

For investors: India’s risk-adjusted edge is intact

The 2021 mania is gone (good), but the structural edge remains: massive domestic demand, improving infrastructure rails (UPI/ONDC/AA), and a founder base that’s been through at least one real cycle. Tracxn’s data—India as the #3 funded country YTD—backs what your pipeline already suggests: there’s volume and quality here; you just have to do the work.

The bottom line

$7.7B with stricter terms beats $20B with sloppy discipline. India’s startup engine is trading speed for stamina—and that’s a fair trade. If you’re building right now, treat this phase as a recalibration, not a retreat. The global league table still has India near the top; the market is just asking you to earn your place.