Google just made borrowing money feel as casual as ordering biryani.

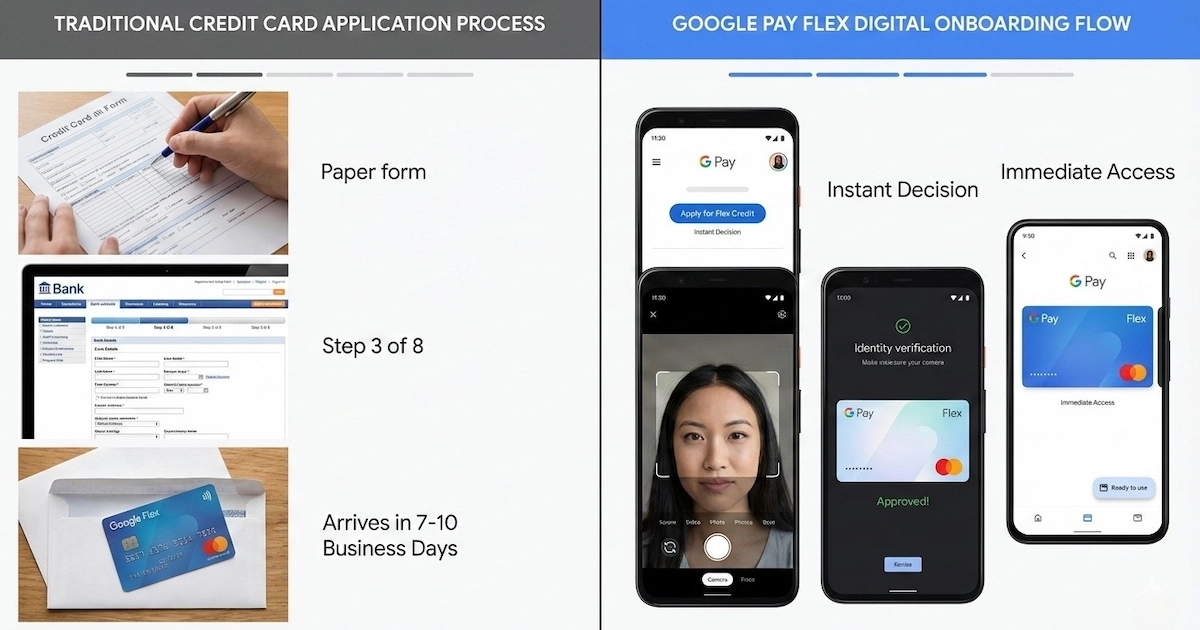

On December 17, 2025, the tech giant launched Flex by Google Pay—a fully digital, UPI-powered credit card in partnership with Axis Bank. Built on the RuPay network, this card lives entirely within the Google Pay app. No plastic. No paperwork. No branch visits. Apply in minutes, start spending immediately.

Sounds like financial inclusion done right. And for some users, it genuinely is.

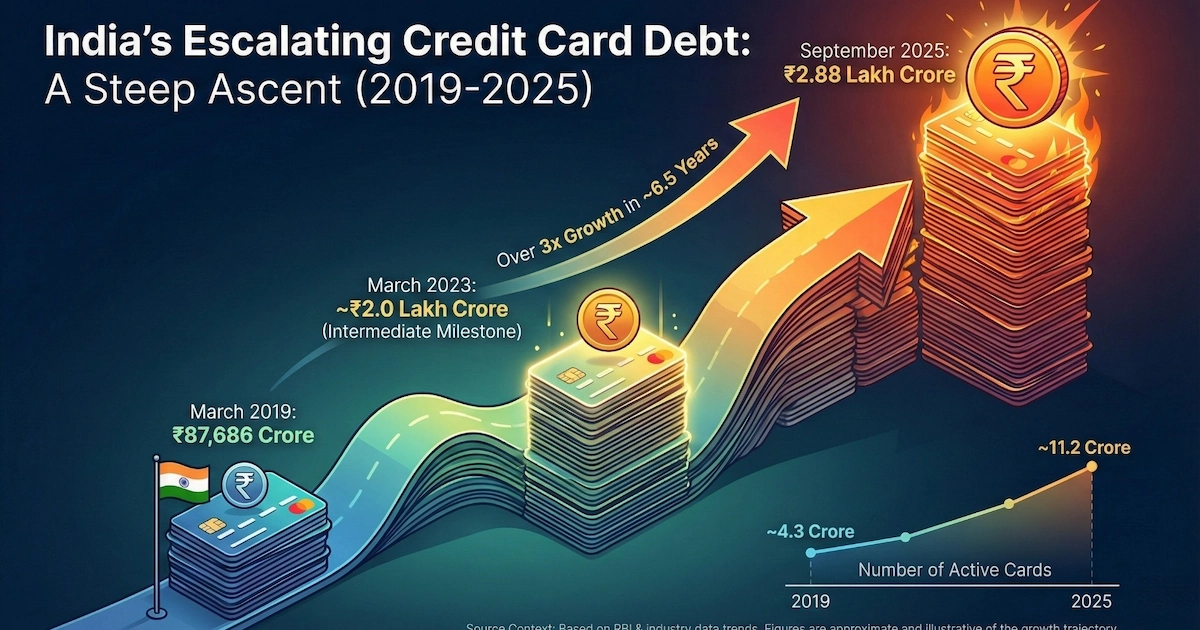

But here's what the glossy press release doesn't mention: India's credit card outstanding has surged over 84,000% in the last decade, hitting ₹2.88 lakh crore by September 2025. And according to Financial Times estimates, roughly 40% of Gen Z in India are already battling unsustainable debt across loans and cards.

So when Google says it wants to "reimagine everyday credit for the next generation," the question worth asking is: which version of that generation's future are we building?

What Exactly Is Google Pay Flex?

Flex is a co-branded RuPay credit card that works through UPI. Think of it as your regular credit card, but instead of swiping or tapping a physical piece of plastic, you scan a QR code—the same motion you already use to pay for everything from groceries to rent.

The key features include:

Instant Digital Onboarding: Apply within the Google Pay app with no physical documentation. Approval and card issuance happen in minutes. No branch visits, no waiting for couriers.

UPI-Native Payments: Pay at any merchant accepting RuPay or UPI—which is essentially everyone. Online apps, offline stores, your neighbourhood kirana—all accessible through your credit line.

Stars Reward System: Earn "Stars" on eligible transactions (1 Star = ₹1). Start at 2X rewards, unlock 4X when spending exceeds ₹15,000 in a reward cycle. Redeem instantly against your next payment.

Flexible Repayment: Pay the full bill, the minimum due, or convert purchases into EMIs (3 to 12 months) directly within the app.

In-App Controls: Set spending limits, block/unblock the card, reset your PIN, and monitor transactions—all from Google Pay.

The card launches with a waitlist system, rolling out to all users over the coming months. Welcome rewards include a ₹250 gift card and 250 Stars.

"We built Flex to bridge this gap, simplifying and reimagining the card experience for the next generation of users," said Sharath Bulusu, Senior Director of Product Management at Google Pay.

Why Google Is Betting Big on Credit

The numbers explain the opportunity.

India has over 530 million unique UPI users making digital payments monthly. But credit card holders? Just about 50 million—roughly one in every 28 Indians. That gap between digital payment adoption and credit access is precisely where Google sees gold.

Consider this: UPI transactions crossed 14 billion in August 2025 alone. When you already own the rails people use for everyday payments, adding a credit layer means monetizing every chai, every grocery run, every Swiggy order. The merchant discount rate (typically 1-2% on transactions over ₹2,000) flows directly to the ecosystem.

Google isn't alone here. PhonePe launched its co-branded RuPay credit card with HDFC Bank in June 2025 and followed up with SBI Cards a month later. Paytm has been in this game since 2019 with Citibank. Cred and super.money offer similar UPI-linked credit products.

But Google brings something others don't: a 530-million-user head start and integration with Maps, Search, YouTube, and the broader Android ecosystem. If you're already living inside Google's world, Flex feels less like a new product and more like an obvious extension.

The Genius: Frictionless Credit Done Right

Let's give credit where it's due (pun intended).

For financially literate users, Flex is genuinely excellent. The rewards are competitive—4X Stars on high spending translates to meaningful cashback. The in-app controls eliminate the anxiety of lost cards or forgotten due dates. The EMI conversion feature adds flexibility for large purchases without visiting a bank branch.

The zero-documentation onboarding democratizes access. Traditional credit cards require salary slips, ITR copies, address proofs—paperwork that excludes gig workers, freelancers, and the informally employed. Flex's digital KYC process opens doors that were previously shut.

Transparency is built in. Interest rates, EMI breakdowns, and processing fees appear on-screen before you confirm. No fine print buried in page 47 of a terms document.

And the security features are robust. Transaction limits, instant card blocking, PIN resets, and tokenization (merchants receive encrypted codes, not your actual card number) address legitimate fraud concerns.

For someone who pays their credit card bill in full every month, never touches the minimum due option, and uses credit strategically for rewards and cashback—Flex is a no-brainer upgrade.

The Trap: When Convenience Becomes a Problem

Here's where it gets complicated.

"UPI has made debt invisible," says Kundan Shahi, founder of Zavo, a platform helping consumers settle unsecured debt. His company's data reveals that 13% of their users are only paying the minimum balance on their credit cards—a behaviour that triggers compound interest spiralling into the 36-42% annual range.

Even more concerning: "When it comes to RuPay-UPI linked cards, we're seeing credit card spending shift to chai, groceries, and even ₹10-₹20 items—things you'd never swipe a physical credit card for."

This is the core paradox. The friction of pulling out a plastic card, the psychological "pain of paying," the momentary pause before a purchase—these aren't bugs in the traditional credit system. They're features. They create micro-moments of financial reflection.

When buying becomes as thoughtless as tapping a QR code you already tap 20 times daily, that reflection disappears. And for young consumers still building financial discipline, that disappearance is dangerous.

The data backs this up:

- 70% of iPhones in India are purchased on EMIs

- 27% of vacations are financed through credit

- 75% of purchases during online sales are made via EMIs

- Credit card debt has spiked 44% in just one year

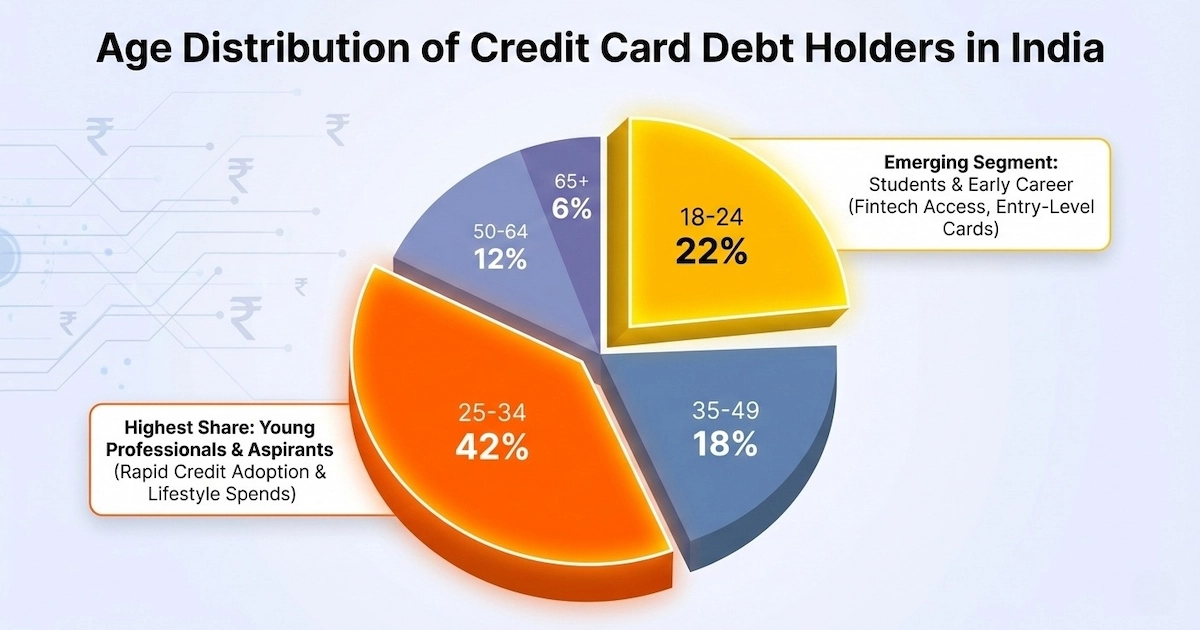

Much of this growth is concentrated among users aged 18-34, the exact demographic Google is targeting as "the next generation of card users."

What the Numbers Actually Say About Gen Z and Debt

According to TransUnion data, the average credit card balance for consumers aged 22-24 is ₹2,834 today—compared to an inflation-adjusted ₹2,248 in 2013. Gen Z already carries more credit card debt than previous generations did at the same age.

Between March 2022 and February 2024, the share of Gen Z users with subprime credit scores (below 600) jumped 8 percentage points to 33%, per Credit Karma data.

A user shared on Reddit: "I've accumulated around ₹1.5 lakh in credit card dues. After reviewing my expenses, I realised I'd actually spent only about ₹80,000-85,000—the rest is all interest."

This isn't an outlier story. It's increasingly common.

The RBI has noticed. In November 2023, the central bank increased risk weights on credit card receivables to 150% for commercial banks (up from 125%), forcing lenders to set aside more capital for every rupee lent on cards. New regulations in 2025 mandate explicit OTP-based consent before issuing any credit card and require dispute resolution within 30 days.

But regulatory guardrails work only when consumers understand what they're guarding against. And that's where the gap persists.

The EMI Illusion and Minimum Due Trap

Flex prominently offers EMI conversion as a feature. Convert your bill into 3, 6, 9, or 12-month instalments. Sounds helpful. Often, it isn't.

Here's the math most users don't calculate: A ₹12,000 phone purchase converted to 12 EMIs at typical credit card interest rates (18-24% annually) ends up costing ₹13,200-₹13,800. That's a 10-15% premium for the convenience of spreading payments.

Worse is the minimum due trap. If you owe ₹10,000 and pay only the minimum (typically 5% or ₹500), you avoid late payment fees. But the remaining ₹9,500 starts accruing interest—often at 3-3.5% monthly, which compounds to 36-42% annually.

Pay only the minimum for six months on a ₹10,000 balance, and you could owe more than you started with despite making payments every single month.

"These numbers are an alarm bell," Shahi told The Core. "Most users don't realise that minimum due is not relief—it's a trap."

Who Should Actually Get This Card?

Flex makes sense if you:

- Already use credit cards and pay in full every billing cycle

- Want to consolidate UPI convenience with credit rewards

- Prefer digital controls over branch visits

- Understand the difference between credit limit and spending budget

- Have a stable income with emergency savings covering 3-6 months of expenses

Flex is risky if you:

- Have ever rolled over a credit card balance to the next month

- Shop impulsively during flash sales and deal days

- Use credit to cover essential expenses your income can't handle

- Don't track your monthly spending or maintain a budget

- Confuse "available credit" with "money you have"

There's no judgment here—just math. If you're in the second category, plain UPI from your savings account keeps spending directly tied to what you actually possess.

The Regulatory Landscape and What's Coming

The RBI has been tightening norms around digital lending since 2022. Key interventions include:

- Prohibiting non-bank PPI issuers from loading prepaid wallets through credit lines (June 2022)

- Mandating explicit consent via OTP before credit card issuance (2025)

- Increasing risk weights to make credit card lending more expensive for banks

- Requiring banks to update credit records fortnightly instead of monthly

New risk-based authentication rules taking effect in April 2026 will require two-factor authentication for all digital payments, with biometric options supplementing SMS OTPs.

But regulation remains reactive. As EY noted in an analysis of UPI credit integration, the merchant discount rate on credit-based transactions creates tension with UPI's zero-cost ethos for merchants. Small businesses with thin margins may disable credit-on-UPI payments entirely, fragmenting the seamless experience Google is promising.

The Bottom Line

Google Pay Flex is an exceptionally well-designed product solving a real problem—India's massive gap between digital payment adoption and credit access. For users who understand credit and wield it responsibly, Flex offers genuine value: competitive rewards, superior convenience, and transparent controls.

But design this good creates its own danger. When borrowing feels indistinguishable from spending your own money, the psychological guardrails that prevent overspending crumble. For Gen Z users still establishing financial habits, that crumbling could set them back years.

The genius and the trap are the same feature.

Whether Flex becomes a tool for financial empowerment or a gateway to debt depends entirely on who's tapping that QR code—and whether they understand what's actually happening when they do.

We'll update this piece when Google announces additional issuer partnerships and when Axis Bank publishes detailed interest rate schedules for Flex users.